Wednesday, 05 April 2006 22:25

Purpose-Oriented Reporting for Aftersales Operations

When I meet my friends who made huge investments in automotive sector and get the dealerships of various brands, the conversations always focus on servicing and spare-parts activities. Profit on vehicle sales falls down on one hand, and sales/marketing expenses rise on the other hand, due to internal and external competition. For his reasons, the ones, who have invested capital on dealership in automotive sector, attemp to operate in almost every branch of the sector and increase their total revenues. The relationship, which is initiated for vehicles sales, carries on with purchase of the customer’s vehicle, car and traffic insurances, extended warranty, rent-a-car, accessories, service and spare parts.

Service and spare-part activities have remarkable importance for those works complementing each other. The relations proceed after the sales process. Efficient and successful aftersales service performances cause brand loyalty and provide advantage to the company regarding the customer who plans to buy a new vehicle. Considering the fact that acquisition of a new customer is 6-7 times more expensive than keeping the existing customer in hand, customer satisfaction and loyalty within aftersales services become much more important. In addition, aftersales service revenues is like a lifesaver within frequent sharp decrease periods within automotive industry. Many companies, therefore, attempt to satisfy their customers and increase their revenues by creating differences in aftersales services. For this reason, top executives with sales expertise of many authorized dealers improve theirselves in terms of spare parts and service.

Almost all distributors provide a service and spare part operating system (program) to their dealers. Using this system, dealers save all performed operations into their computers and generate many reports by means of those saved datas. The number of opened work orders within relevant month is supplied with fractions of mechanics, hood etc, efficiency and productivity of personnel is examined in details, the spare parts volume and labour revenues per work order are listed, the number of types of vehicles which are provided service is determined within those reports. Those systems are used to working like a report factory at the end of each month. Then, generated reports are presented to the executives of dealers. And this is the start point indeed. The executives study those report and understand the facts and figures. Sometimes they lose their ways within those reports and try to find an executive who is experienced in service and spare parts.

Eliyahu Goldratt states “The main goal of the company is to make profit.” within his very own book “The Goal”. When such an approach is adopted, as Goldratt stated, a common and collective goal is created within the company in case the goal is expressed by easily understandable terms. Let’s give an example to clarify the point; the number of the serviced vehicles is 500, our staff productivity is 75%, the availability rate is 90%; those figures do not mean so much for the top executives. In other words, top executive should be provided the results of goal-oriented works for a better understanding. I, therefore, suggest the top executives, who are in charge of service and spare part operation, to focus on three main facts- sales, (spare part and service), stock and general expenses- in order to examine current situation and conditions. Sales volumes should be increased whereas stock level and general expenses should be decreased for a successful operation. Higher sales volume means more serviced cars and higher sales volume per work order. Also, reduced stock figures mean higher stock circulation coefficent, whereas increased general expenses mean less staff performance and also higher phone, electricity, water etc expenses. Almost all required informaton is usually available for monitoring/following of those three basic indicators. Top executives shall be able to see the overview of operation as soon as they review sales, stock and general expenses figures within the system.

Unless the values are not obtained from this system, the following model can be used:

Sales

1. Spare-part sales revenue (in-service)

2. Spare-part sales revenue (out of the service workshop)

3. Revenus on consumables such as oil, grease etc

4. Workmanship/labour revenue

5. Total revenue (1+2+3+4)

2. Spare-part sales revenue (out of the service workshop)

3. Revenus on consumables such as oil, grease etc

4. Workmanship/labour revenue

5. Total revenue (1+2+3+4)

Inventory/Stock

6. Total amount of spare parts as of the end of month

7. Total amount of consumables revenues such as oil, grease etc as of the end of month

8. Total cost of sold spare parts as of the end of month

9. Total cost of consumable revenues such as oil, grease etc as of the end of month

10.Total stock (6+7)

7. Total amount of consumables revenues such as oil, grease etc as of the end of month

8. Total cost of sold spare parts as of the end of month

9. Total cost of consumable revenues such as oil, grease etc as of the end of month

10.Total stock (6+7)

General Expenses

11.Salaries of service technicians (11a+11b)

11.a. Mechanics and electrician salaries

11.b. Hood technician and painter salaries

12.Customer consultant salaries

13.Salaries of spare-part staff

14.Salaries of service and spare-part manager

15.Other salaries (security, cleaning staff etc)

16.Electricity expenses

17.Communication expenses such as phone, mail, sms, etc

18.Water and cleaning expenses

19.Rental expenses

20.Total general expenses (11+12+13+14+15+16+17+18+19)

21.Gross profit [5-(20+8+9)]

11.a. Mechanics and electrician salaries

11.b. Hood technician and painter salaries

12.Customer consultant salaries

13.Salaries of spare-part staff

14.Salaries of service and spare-part manager

15.Other salaries (security, cleaning staff etc)

16.Electricity expenses

17.Communication expenses such as phone, mail, sms, etc

18.Water and cleaning expenses

19.Rental expenses

20.Total general expenses (11+12+13+14+15+16+17+18+19)

21.Gross profit [5-(20+8+9)]

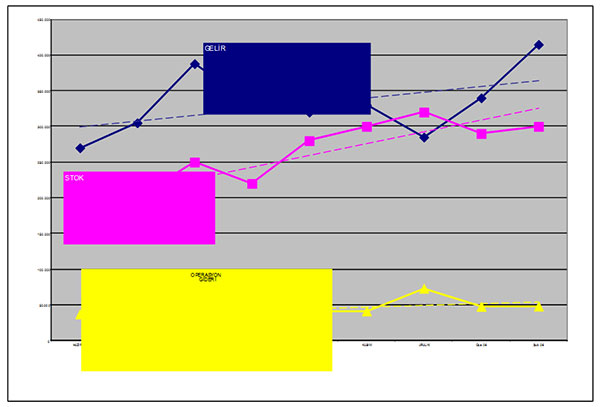

It will be so useful to see the information above on a chart after preparing them per month. Yet, it will also help to make an analysis of sales, stock and general expenses trends success and the points to be improved within aftersales operation. For instance, sales, stock and general expenses rises in the same time within the following chart.

An executive who reviews this chart shall not focus on increased sales volume but increased stock and general expenses. Unless stock and general expenses are increased in compliance with increased sales volume, in other words, unless stock and general expenses are increased due to a specific reason, the executive will take required measures to divert those expenses. Inactive stocks shall be examined and also stock circulation coefficent, and, stock/month figures shall be checked for active stocks in order to divert the increased stock. Moreover, the first point to be focused on within increased general expenses shall be the salaries. In case the reason of increase is as a result of salaries, performance analysis should me made after examining whether employment and overtime work levels are increased or not. In case of a decrease in sales volume, the number of serviced cars, spare parts and labour revenues per work order shall be examined to provide crucial and efficient datas for the executives.

After all; top executive shall be able to clearly see and realize what to do by means of goal-oriented reporting within aftersales operations. Since the executives, who aim to make profit on spare parts and service fields, keep sales, stock and general expenses under control, all staff would be able to act in compliance with the goal.